By using this website, you agree to the use of cookies as described in our Privacy Statement.

You also confirm you understand that the information on this site is intended as a guide only. The information is of a general nature and does not and cannot ever constitute personal advice.

In New Zealand serious illness is 2.6 more times more likely to strike than a serious accident putting an earner off work for six months or more.

The accident victim will get 80% of income from Accident Compensation. The illness victim without income protection will have their household income means tested before they are eligible for a sickness benefit. A couple with or without children on the M tax rate will have to fall back on a sickness benefit paying about $341.60 a week.

Most two-income families have a second earner whose income would preclude them from receiving a sickness benefit.

Only about 15% will have income protection insurance, whereas 100% have coverage for accident through ACC.

Every seventh home with an income earner can tell a story of the main earner falling seriously ill and being off work for six months or more during the past five years, according to new research.

On average, here is what will most likely happen at households out across New Zealand after annual and sick leave and savings run out where there is no income protection and serious illness puts the income earner off work for six months or more, according to new research …

Fidelity Life was founded in 1973 by two Kiwi's, Gordon and Shirley Watson. Since then have paid out over $1.4B in claims to Kiwis.

Fidelity Life are supported by shareholdings from the NZ Super Fund and Ngāi TahuHoldings. These investor's multi-generation investment horizons ensure decisions will continue to be made for New Zealanders, by New Zealanders, for years to come.

We can offer you assistance with Fidelity Life Personal insurance policies.

On Fidelity Life's YouTube page you can view helpful videos explaining the different types of insurance they offer and heart warming stories from people who's have made insurance claims.

Life insurance can seem daunting at first, but it's one way to help safeguard the financial future of yourself and your family if something were to happen to you.

Not insured?

Getting yourself covered can start right here.

Explore our range of easy to understand and plain-English insurance 101 guides, packed full of videos and blog content, to help you learn about what protection you may want to consider.

Disclaimer: the information contained in this video is a summary of the key points of this insurance cover and is general in nature, it does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. Any references to benefits made in this material relate to Fidelity Life’s current on-sale policy wording, and may not be accurate in respect to older policies. All applications for cover are subject to underwriting criteria.

Wherever you’re at in life, it’s likely someone relies on you being around and staying healthy. Have you ever thought how you or your loved ones would get by without your income? Life insurance is a way to protect the financial future of you and your loved ones in times of sickness, injury or when you die.

Not insured?

Getting yourself covered can start right here.

Explore our range of easy to understand and plain-English insurance 101 guides, packed full of videos and blog content, to help you learn about what protection you may want to consider.

🡆 Visit our life insurance 101 blog: fidelitylife.co.nz/insurance-101/

🡆 Or get in touch with a financial adviser today to discuss what types of insurance cover are right for you: www.fidelitylife.co.nz/contact/get-in-touch/

Disclaimer: The information contained in this video is a summary of some key points about different insurance covers. This information is general in nature and this video does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. All applications for cover are subject to underwriting criteria.

There are different types of life insurance that are designed to protect you from different things. All of them aim to safeguard you and your family’s financial future from things that might happen one day, like sickness, injury, or when you die.

Not insured?

Getting yourself covered can start right here.

Explore our range of easy to understand and plain-English insurance 101 guides, packed full of videos and blog content, to help you learn about what protection you may want to consider.

🡆 Visit our life insurance 101 blog: fidelitylife.co.nz/insurance-101/

🡆 Or get in touch with a financial adviser today to discuss what types of insurance cover are right for you: www.fidelitylife.co.nz/contact/get-in-touch/

Disclaimer: The information contained in this video is a summary of some key points about different insurance covers. This information is general in nature and this video does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. All applications for cover are subject to underwriting criteria.

Buying a house is a big deal and it often comes with the increased financial responsibility of a mortgage to repay. Life insurance could protect your ability to pay off some or all of the mortgage if a sickness, injury or something worse prevents you from working.

Not insured?

Getting yourself covered can start right here.

Explore our range of easy to understand and plain-English insurance 101 guide, packed full of videos and blog content, to help you learn about what protection you may want to consider.

🡆 Visit our life insurance 101 blog: fidelitylife.co.nz/insurance-101/

🡆 Or get in touch with a financial adviser today to discuss what types of insurance cover are right for you: www.fidelitylife.co.nz/contact/get-in-touch/

Disclaimer: The information contained in this video is a summary of some key points about different insurance covers. This information is general in nature and this video does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. All applications for cover are subject to underwriting criteria.

When you have a family, protecting them is often your number one priority. Life insurance can be a sensible way of taking steps to provide for them financially if anything happens to you.

Not insured?

Getting yourself covered can start right here.

Explore our range of easy to understand and plain-English insurance 101 guides, packed full of videos and blog content, to help you learn about what protection you may want to consider.

🡆 Visit our life insurance 101 blog: fidelitylife.co.nz/insurance-101/

🡆 Or get in touch with a financial adviser today to discuss what types of insurance cover are right for you: www.fidelitylife.co.nz/contact/get-in-touch/

Disclaimer: The information contained in this video is a summary of some key points about different insurance covers. This information is general in nature and this video does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. All applications for cover are subject to underwriting criteria.

Making a claim can feel overwhelming, and that’s okay. We aim to make the process as smooth as possible, starting by making sure you know exactly what to expect if you ever need to make a claim.

Explore our range of easy to understand and plain-English insurance 101 guides, packed full of videos and blog content, to help you learn about what protection you may want to consider.

Disclaimer: the information contained in this video is a summary of the key points of the claims process. The information provided is general in nature. This video does not constitute a financial advice service. Details of definitions, benefits, standard exclusions/limitations, terms and conditions are contained in the full policy documentation which is available from Fidelity Life or your financial adviser who holds a Distribution Agreement with Fidelity Life. All applications for cover are subject to underwriting criteria. Claims specialists may be subject to change where workload or other business matters require it.

One of the most popular forms of personal insurance cover in the developed world is Critical Illness cover - and for very good reasons.

Yet in New Zealand it is still relatively unknown to most of the population, and most New Zealanders are more at risk than they realise.

Trauma Insurance or Living Insurance

Before considering the case for Critical Illness, we should dispel some myths. Critical Illness is often referred to as "trauma insurance", and it becomes an implied understanding that anything that is a "trauma" might be covered. This is not the case, as trying to cover anything that might be traumatic (which could vary enormously from person to person) is nearly impossible to calculate. To make it clear for people wanting insurance to step in while they are alive and suffering from a major critical condition, the insurers provide a list of covered conditions that you are insured for. There can be quite a number of conditions on a Critical Illness policy that would trigger a claim, however the most common claims come from a relatively short list of very serious health conditions. The purpose of this type of cover is to provide money to people when they need it most, after suffering a specified major health problem - and still being alive. It is sometimes known as "living insurance" for that reason.

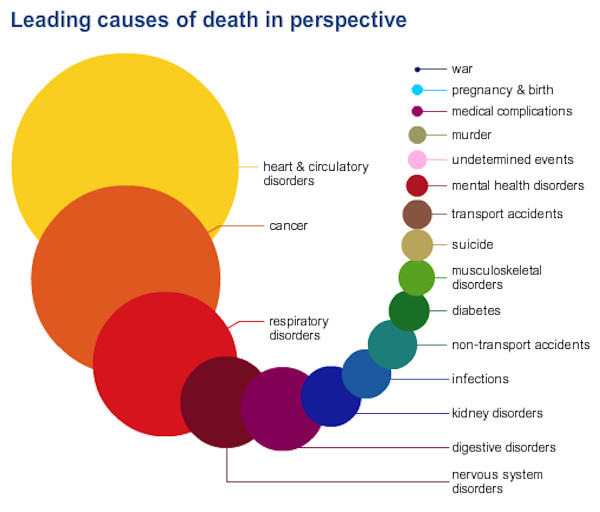

Generally people are terrible at assessing risk. Worrying about having an accident, whilst lighting up another cigarette or eating another plate of chips.

The UK national Health Service put together the Atlas of Risk, a tool to help the English understand the diseases and conditions that are the biggest killers in England and so hopefully make better life style choices.

The comparitive figures are likely to be pretty similar in New Zealand.

“It’s easy to lose perspective and worry about small or insignificant risks while ignoring, or being unaware, of the major threats,” the NHS explains on the site. “The NHS Choices Atlas of Risk has been designed to help put health threats into perspective.”

Provides a lump-sum payment if you are totally and permanently disabled and can't work. Disability insurance cover gives you financial assistance when you need it most, to spend any way you choose.

Why do you need Disability Insurance Cover?

If you become completely and permanently disabled through an accident or an illness, you may receive limited ACC cover and a basic sickness benefit.

Would this be enough to cover your current living expenses and allow you to plan for your future?

Probably not !

In addition to losing your income, you may be facing extra costs to assist with your daily living, whether it's alterations to your home or paying for the care that you may need.

A lump-sum payment will allow you to pay off debt and set yourself up for the future. You will have the financial freedom to live your life to its fullest potential and to make your own choices about the care or treatment you require.

Disability Cover is simple because it is payable irrespective of what has happened to you, this means that if you are completely and permanently disabled and unable to work, your cover will be paid, regardless of what injury or illness you may have suffered.

You can insure against your chosen occupation, which means that you will be paid if your disability is such that you can never work again in that field (available for most occupations) or you can choose to insure against the possibility of never being able to work again in any occupation for which you are suited.

Some of the features available are

Your benefit is not offset against ACC payments. The cover can pay you the full benefit regardless of any ACC payment, putting more in your pocket when you need it most.

Additional cover for a range of 'lifestyle events' e.g. if you get married, have a baby or buy a new house etc, which allows you to keep your insurance up to date with your changing lifestyle, regardless of any changes to your health.

You can 'Accelerate' your benefit against your Life Cover – at claim time your Life Cover will be reduced by the amount of your claim which will reduce your premium.

Options are available to 'buy back' your lost Life Cover. At a time when your health has been severely affected, you have this opportunity, giving you and your family added financial security at a time when it would be very difficult to get more life insurance.

To discuss Disability Insurance or any of your other insurance needs please phone Phil Sedcole on 07 578 3863 or Freephone 0800 867 323.

Did you know?:

Stroke is the major cause of adult disability in New Zealand. 8,000 adult New Zealanders suffer a stroke each year (a third of which are fatal). There are 56,000 stroke survivors in New Zealand, many of whom have disability and need significant daily support. Each year a quarter of all stroke victims will be under retirement age. (Stroke Foundation of New Zealand, 2008)

Income Insurance pays a monthly benefit if you are unable to work because of a total disability.

Ask yourself this –

If you had an accident or became very ill and were no longer able to earn an income, how would you manage financially?

In some circumstances you may receive financial assistance from the Government. The bad news is that it's unlikely to be enough to maintain your current lifestyle, let alone allow you to plan for your future – pay off the mortgage, your children's education, retirement savings, holidays etc.

Income Cover provides you with a regular income, allowing you to live the life you want to live. You will remain financially independent, regardless of whether or not you are able to return to work.

Most people take it for granted that they will work until they can afford to retire – and for many of us that means we will still be working until we are at least 65, when government super commences.

It's worth thinking about how much you are likely to earn over your lifetime - because if something happened and you were unable to work, then that's how much you risk losing.

For example:

Let's say you are 30 years old and you earn $60,000 per annum. You have an Income Cover policy worth $45,000. If you suffered a total disability and were unable to work, here's an idea of how much income you would lose - and how much your claim would be worth:

Imagine if your employer gave you choice in the salary package that you could take.

For example, what if you were given the following to choose from?

a. Annual Salary = $50,000 plus 4 weeks annual leave, plus 7 days annual sick leave; OR;

b. Annual salary = $48,500, plus 4 weeks annual leave, plus 7 days annual sick leave PLUS 75% of your income is guaranteed until age 65 if you get too sick (or hurt) to be able to come back to work again.

Think about your choice carefully.

You could get paid the top salary and take all the risk yourself of being able to go to work each day and continue earning an income. Or you could forego a little of the income – but not your other employment benefits – in return for a guarantee that regardless of what happens to your future health you will keep earning money through your working life.

That is an enormous amount of potential risk that you can pass to somebody else if you want to, or you can choose to keep all the income and all the risk for yourself.

Put some simple numbers around it to help weigh up the options. If you are 45 and earning $50,000 p.a. through until age 65 then that is an even $1,000,000 in future income at risk – all dependent on you staying healthy and being able to go to work of course. Would you be willing to trade perhaps 3% of that to secure most of your future income for the rest of your working life?

We take our ability to work very much for granted, even though we often wish for the day when we don’t have to work. Getting to that day when we no longer have to work is going to depend on our ability to keep working, earning and saving however – and this is where income protection comes in.

Imagine if you couldn’t work because of illness and suddenly your income stops after just a few short weeks. Many New Zealanders will be worrying within a month about where the money will come from for the mortgage, electricity, phone, rates, food, the list goes on. You would quickly forget about the plans you had for holidays, entertainment, future lifestyle choices and and purchases.

There is no doubt that for the majority of people the ability to work and earn and ongoing income is their single biggest asset.

One of the problems we create for ourselves too is that the more we earn the more our lifestyle expectations increase...the more we spend on having a better life.

Maybe we think of ourselves as indestructible, but statistics tell us we are far more likely to have a disability lasting more than three months than we are to have our house burn down. Yet we pretty much all insure our house...and cars...

Assessing the risk here is relatively simple. If we assume that as of today your income stops, it is simply a matter of working out if you can meet your commitments from a sickness benefit? There is the question of course as to whether you’d actually qualify for a sickness benefit – what if you are a double income family and only one income stopped because of sickness? Would it matter which income stopped? If you are single would you have to move in with your parents or live in a boarding house with others that cannot afford to live independently?

That is the risk in its simplest terms. If you want to reduce that risk you need to consider income protection insurance, which (in general terms) will provide you with an agreed amount or proportion of your lost income in the event of being unable to work due to illness or accident.

Once you decide to look into getting some income protection cover though, it gets complicated and there is absolutely no substitute for working with a professional adviser who understands the difference in types of contracts and how they would work at claim time. No two products are exactly the same. And it is not as simple as “any Income Protection is going to suit you”. Some will not suit you and your circumstances at all.

Some of the factors that will affect the choice of what income protection cover will work best for you will be things like:

Whether you have a salary or are self-employed

How much you have in savings, investments, leave entitlements

If your income fluctuates from year to year

If you get fringe benefits you rely upon (e.g. get a company car?)

Do you have business expenses that continue while you are disabled

Do you split your income for taxation purposes

Even with the help of a professional adviser who can work out which contract is most likely to be right for you and work at claim time, there is no guarantee that the cover you selected will be right forever more. You have to review it regularly and make sure the cover you chose is still going to be the cover that works for you.

Before considering the case for Critical Illness, we should dispel some myths. Critical Illness is often referred to as "trauma insurance", and it becomes an implied understanding that anything that is a "trauma" might be covered. This is not the case, as trying to cover anything that might be traumatic (which could vary enormously from person to person) is nearly impossible to calculate. To make it clear for people wanting insurance to step in while they are alive and suffering from a major critical condition, the insurers provide a list of covered conditions that you are insured for. There can be quite a number of conditions on a Critical Illness policy that would trigger a claim, however the most common claims come from a relatively short list of very serious health conditions. The purpose of this type of cover is to provide money to people when they need it most, after suffering a specified major health problem - and still being alive. It is sometimes known as "living insurance" for that reason.

Before considering the case for Critical Illness, we should dispel some myths. Critical Illness is often referred to as "trauma insurance", and it becomes an implied understanding that anything that is a "trauma" might be covered. This is not the case, as trying to cover anything that might be traumatic (which could vary enormously from person to person) is nearly impossible to calculate. To make it clear for people wanting insurance to step in while they are alive and suffering from a major critical condition, the insurers provide a list of covered conditions that you are insured for. There can be quite a number of conditions on a Critical Illness policy that would trigger a claim, however the most common claims come from a relatively short list of very serious health conditions. The purpose of this type of cover is to provide money to people when they need it most, after suffering a specified major health problem - and still being alive. It is sometimes known as "living insurance" for that reason.

ranteed until age 65 if you get too sick (or hurt) to be able to come back to work again.

ranteed until age 65 if you get too sick (or hurt) to be able to come back to work again.